You can sign up for my newsletter here: eepurl.com/cHA0m9

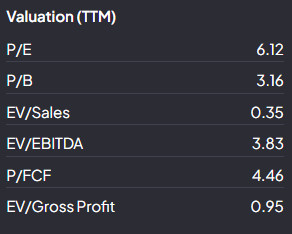

My latest newsletter just went out. This week I've been taking a look at a Bulgarian ship repair yard, a Brazilian sports manufacturer, and a Polish lead-acid battery recycler. The thing they have in common? They all appear exceedingly cheap. thebritishinvestor.com/company-valu...

In recent weeks I've been placing increasing attention on more globally focussed companies (within the scope of my investable countries). My methodology and stock screener is simple: Focus on companie...

Final one. Dutch payment processing company Adyen (ADYEN), currently on a P/E of 53. Five years ago was on a P/E of 116. Even with a less than stellar three year performance has still returned nearly 18% annually in the last five years.

Out of the tech world, Hermes (RMS) shares much the same performance. P/E five years ago was much the same as it is today (mid-high 40's). It's returned 30% a year since.

There's a sizeable chunk of the investing community that would argue Nvidia (NVDA) is overvalued. Three years ago it traded on a P/E of 70. It's returned 77% a year since. Investing is hard.

I go where the value is! Hope you enjoy.

My latest post, in which I've written up three companies for (potential) further investigation. (Valuations included): thebritishinvestor.com/company-valu...

In recent weeks I've been placing an increasing focus on more globally focussed companies (within the scope of my investable countries). My methodology and stock screener is simple: Focus on companies...

My latest post, in which I've written up three companies for (potential) further investigation. (Valuations included): thebritishinvestor.com/company-valu...

In recent weeks I've been placing an increasing focus on more globally focussed companies (within the scope of my investable countries). My methodology and stock screener is simple: Focus on companies...

Shoe Zone PLC likewise, extremely cheap. But again, current liabilities of £30m, and £31m of inventory means that stuff better get sold!

McBride PLC looks absurdly cheap. But that balance sheet... Granted they're reducing net debt but it still isn't one for me.