Indeed! Which is why I recommend smoothing through the noise (to varying degrees depending on the time series in question) and triangulating across as many alternative time series as possible.

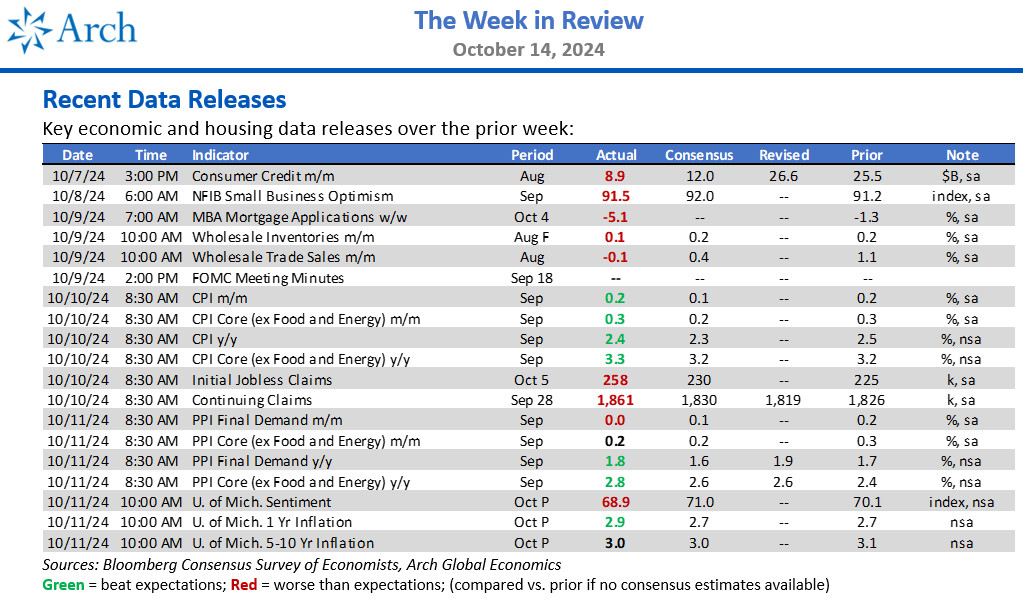

On net, I still expect the Fed to downshift to a 25bps rate cut in November as the disinflationary process remains well underway and risks to the labor market remain skewed to the downside.

Consumer sentiment also soured in the preliminary October UMICH print as year-ahead inflation expectations ticked up to 2.9% from 2.7%.

Jobless claims came in far above expectations, despite most of the increase being driven by non-hurricane factors.

Last week was all about inflation, with a hotter than expected CPI print providing the Fed another reason to dial back the pace of rate cuts.

The week will wrap with an update on the housing market, with the October NAHB Housing Market Index expected to inch higher to 42 from 41 in Sept, while September housing starts and building permits are both expected to tick down modestly.

We'll also get an update on the manufacturing sector with capacity utilization expected to tick down slightly.

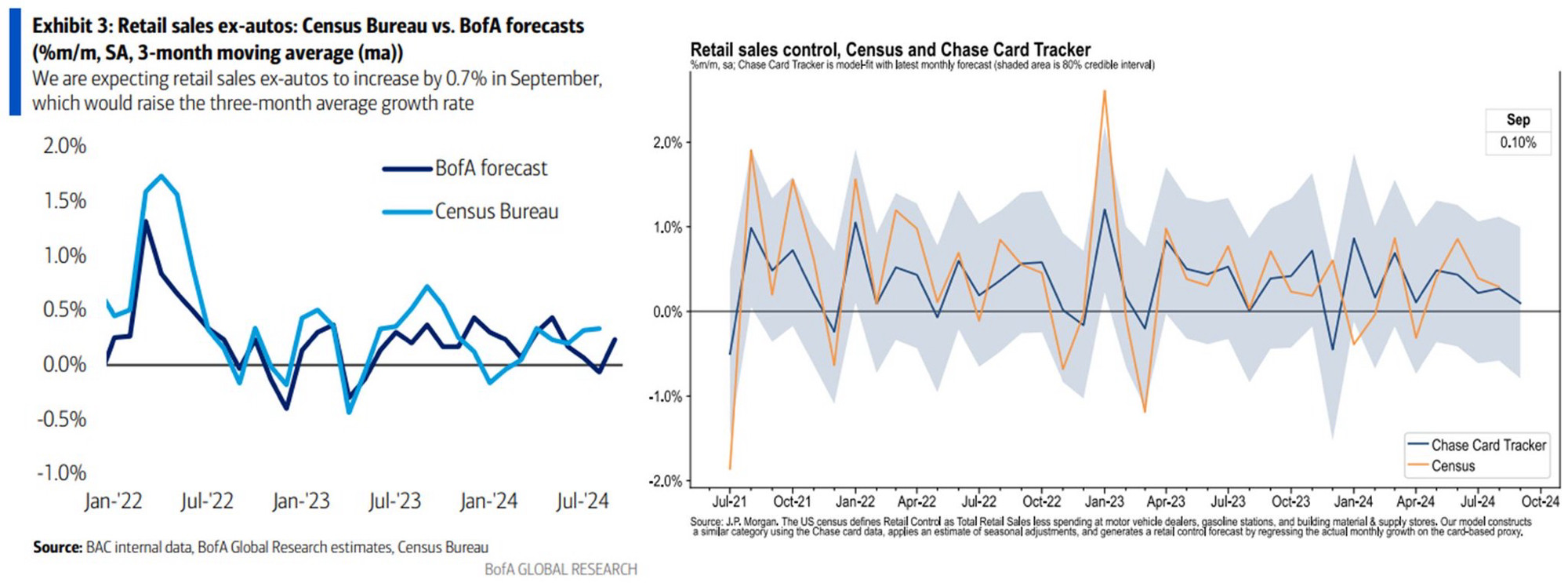

The JPM model has generally fit the Census data a bit better, for what it's worth.

While the BofA card spending data suggests a strong rebound in retail sales excluding autos, the JPM card data suggests a cooldown to modest growth of 0.10% m/m for control group retail sales vs 0.27% prior and consensus of 0.4%.

The Bloomberg consensus survey of economists expects a slight acceleration in September control group retail sales (0.4% m/m sa vs 0.3% prior), but the real-time card spending data is mixed.