The price of this is scandalously low.

Testing for pensions people active here. Can anyone tell me what happens to DC scheme member outcomes if the employer goes insolvent? Do members typically get full benefits somehow or do they typically lose some in sorting out the scheme?

I suspect our children and grandchildren won’t either in many ways. Including the (non-) pension system we are bequeathing them.

Not as interesting for pension nerds as for those interested in other demographically driven public spending.

And that applies whether funded or unfunded.

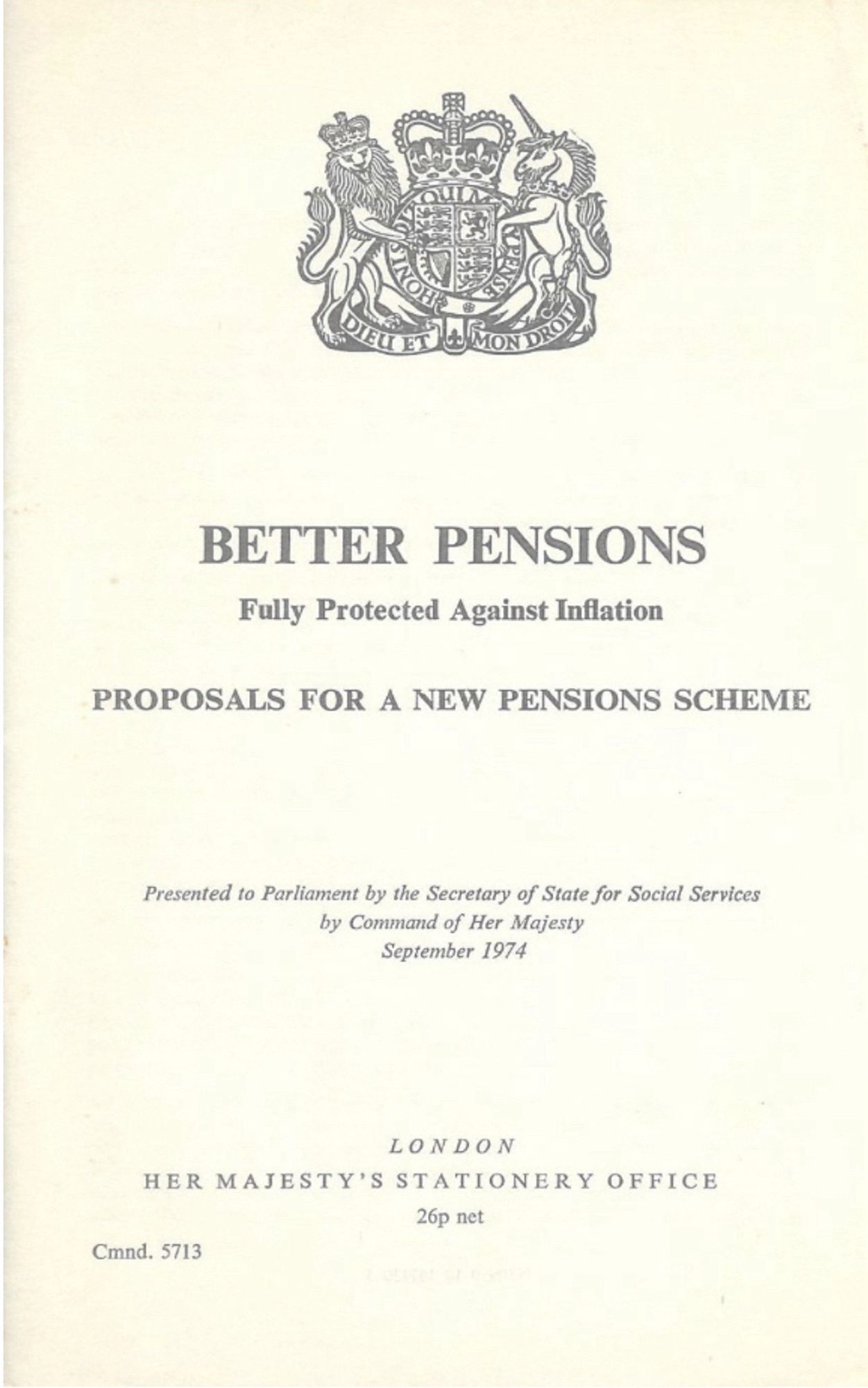

The Barbara Castle/ Labour proposals for Better Pensions are 50 years old this month. We Still Need Better Pensions.

I don’t want low earners to opt out or feel more financial pressure to do so, just prefer them not to be required to oversave. Hopefully the adequacy review will look at this.

I am not so sure low earners need to pay more into inflexible savings accounts, and requiring it from £0 hits them hardest. I am though all for developing sidecar savings and having employers always paying in even if employees opt out. I hope the Review Stage 2 produces AE2.0.

How do pensions cope financially who are potentially eligible to PS but don’t claim? Is this a savings credit issue?