Apologies for not being up on US labour stats recording, but the Labour Force Survey that informs most UK labour stats has been having some real trouble over/after covid. Response rates are right down, making confidence in the data - esp segmented - harder to maintain. Could be having an effect.

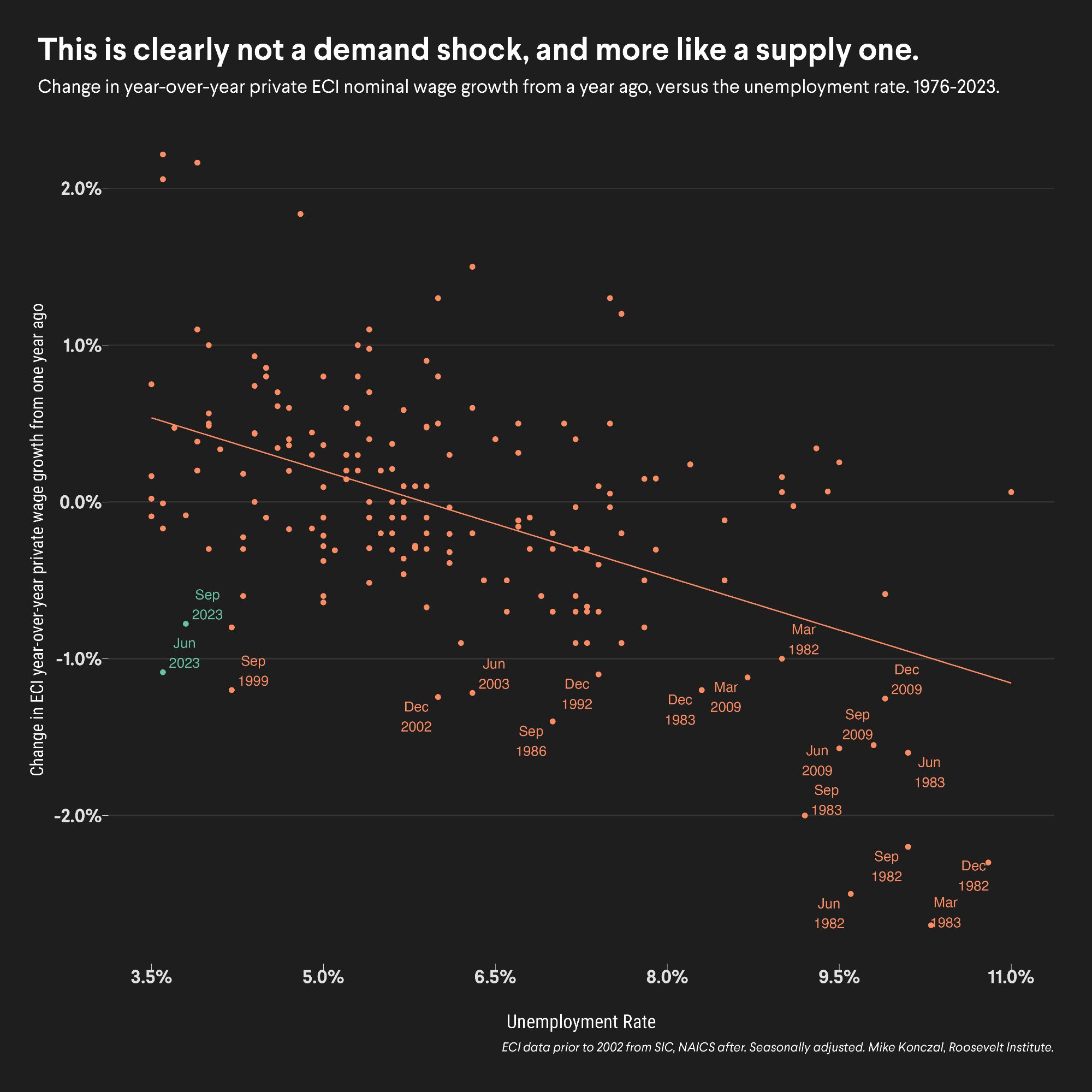

Is it not just anchored inflation expectations combined with the end of a period of real wage resistance? (ie exactly what you’d hope to see with a credible nominal framework.) May be missing the point of the question though.

Exogenous inflation shock(s) and lagging wages.

Does ECI allow you to do any geographical analysis? I would be interested to break out the trend by regions.

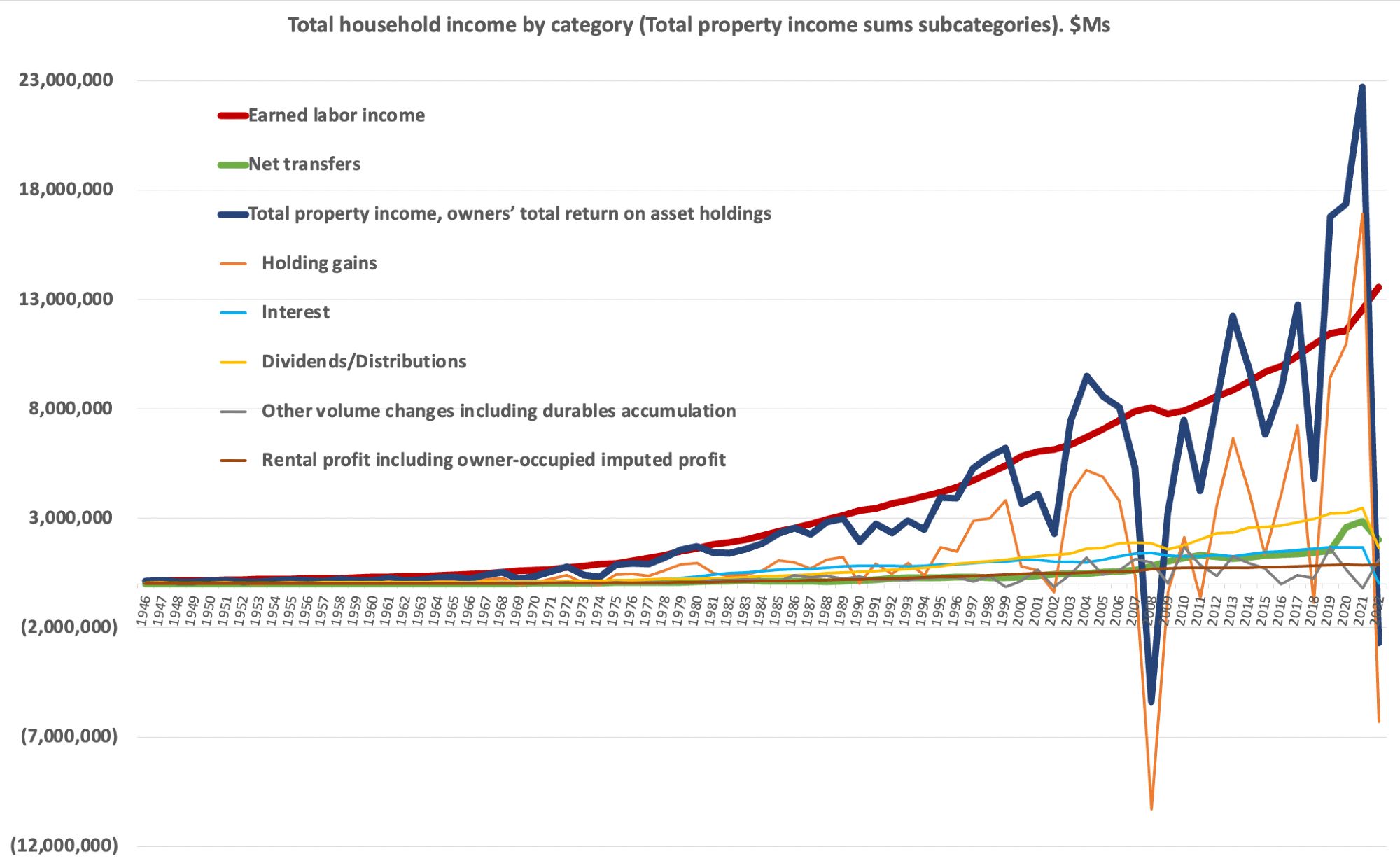

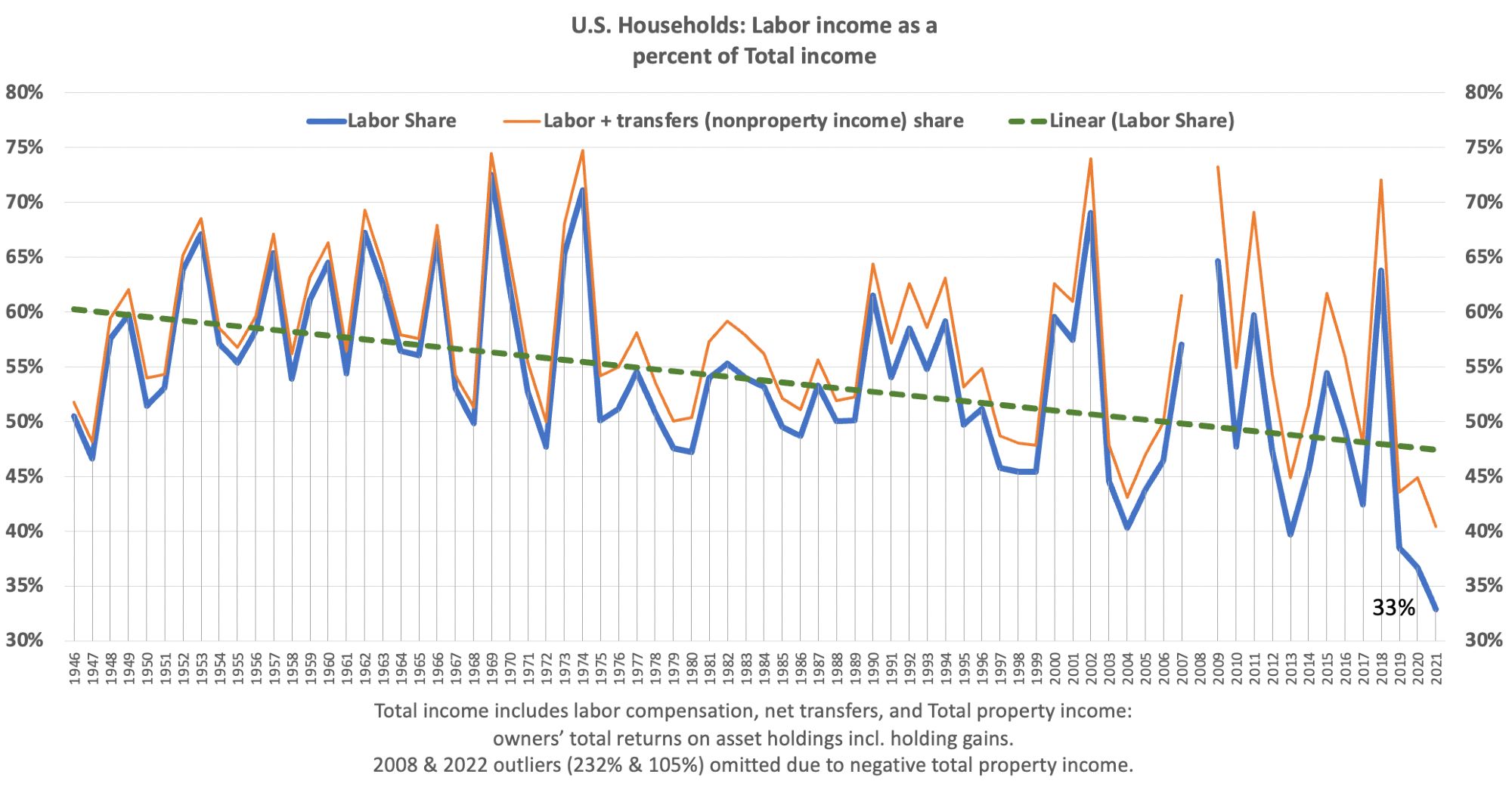

The big jump in the share of Total household income captured by property owners, at workers' expense?

In the canonical NK model, you'd have to interpret it as something else also pushing down on the natural rate of unemployment [benefits, trade union power, mismatch, I think also 'uncertainty' has this effect in het agent models with unemployment].

Companies are hoarding workers rather than let them go, so unemployment looks lower than the actual amount of slack in the labor market. www.reuters.com/markets/us/u...