At a $150bn valuation that’s a 0.33% stake. Masa is so back. www.reuters.com/technology/s...

Japanese telecom company SoftBank's Vision Fund will invest $500 million in OpenAI's latest funding round, The Information reported on Monday, citing a person familiar with the deal.

so factoring in $13 billion of debt the enterprise value has halved? Sounds about right.

oh for sure. But i'm genuinely curious why the Rightmove board is so confident about its standalone future.oh for sure. But i'm genuinely curious why the Rightmove board is so confident about its standalone future.

I get that. But to say no you have to believe the market is wrong about both REA and Rightmove, but in different directions. And if the market is indeed wrong about Rightmove, what is going to prompt a standalone rethink?I get that. But to say no you have to believe the market is wrong about both REA and Rightmove, but in different directions. And if the market is indeed wrong about Rightmove, what is going to prompt a standalone rethink?

yeah I can see why investors might not like the look of REA paper, but you would expect the News Corp holding to be reflected in the price.yeah I can see why investors might not like the look of REA paper, but you would expect the News Corp holding to be reflected in the price.

if that's the case they're leaving it late!if that's the case they're leaving it late!

sure, but REA is offering them a bigger share of the combined group than implied by pre-bid prices. That's effectively a premium.sure, but REA is offering them a bigger share of the combined group than implied by pre-bid prices. That's effectively a premium.

I don't get this. They're employing a "just say no" defence against a buyer offering a 40% premium to the undisturbed price. They have a dominant share of the UK market and a 74% EBITDA margin. What do they think is going to happen to the standalone business that would come close to this valuation?I don't get this. They're employing a "just say no" defence against a buyer offering a 40% premium to the undisturbed price. They have a dominant share of the UK market and a 74% EBITDA margin. What do they think is going to happen to the standalone business that would come close to this valuation?

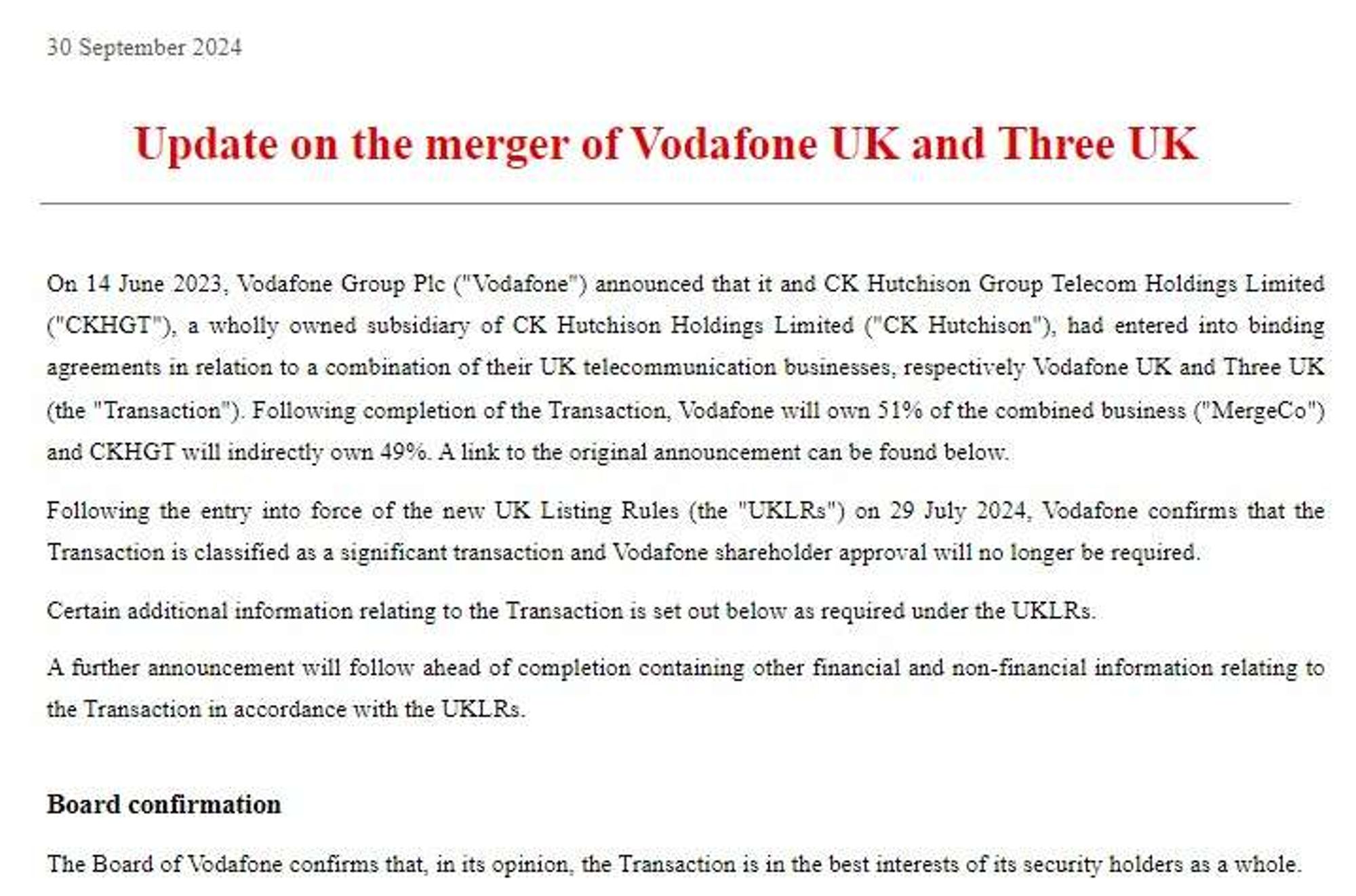

Britain's new "light-touch" stock market listings regime in action: Vodafone shareholders no longer get to vote on merging its UK business with Three.Britain's new "light-touch" stock market listings regime in action: Vodafone shareholders no longer get to vote on merging its UK business with Three.