This likely has real consequences. When firms maintain stable payouts despite declining profits, they must either resort to cutting investments, R&D expenditures, or labor costs or to taking on higher levels of (unproductive) debt.

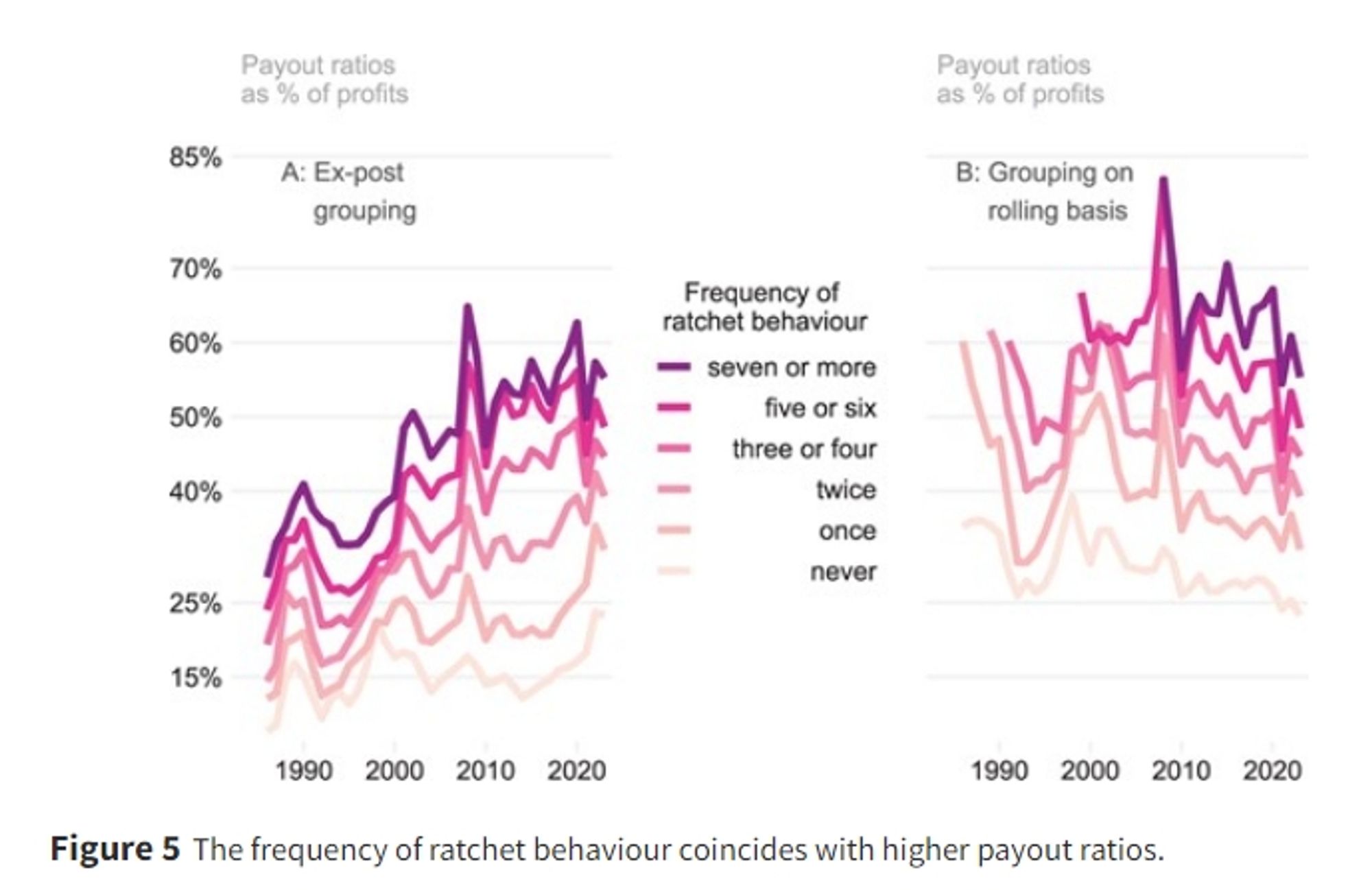

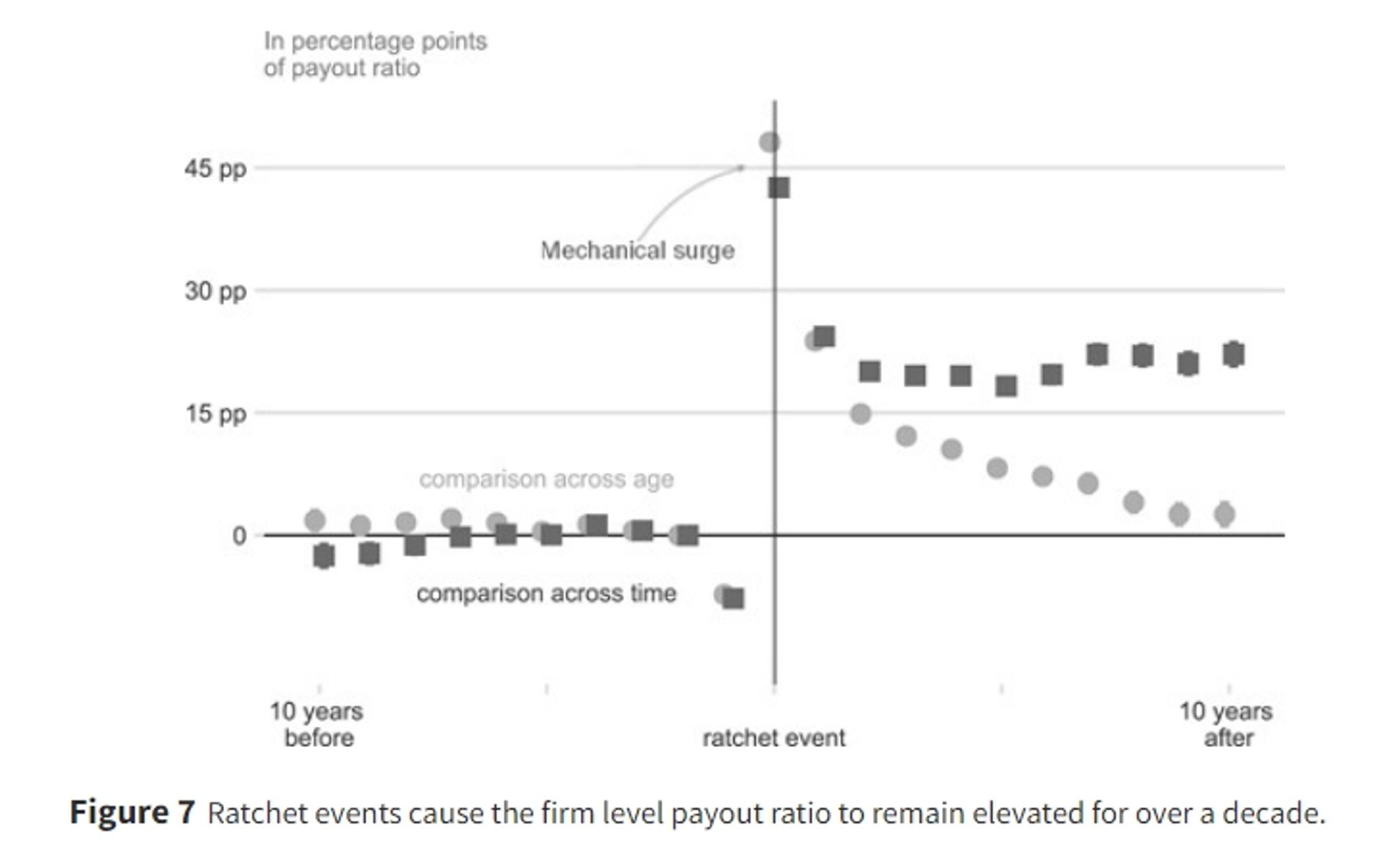

Payouts fractionally adjust upwards in good times but are downward rigid in bad times - just like a ratchet. 1) Aggregate payout ratios are structured along the frequency of ratchet behaviour 2) At the firm level each ratchet event persistently raises the payout ratio for a decade (staggered DiD)

Short summary: bakoumertens.quarto.pub/bakoumertens... People tend to focus on large increases in dividends or share repurchases (payouts), but I show that it is not rising payouts that should attract our attention, but rather their inability to fall.

My first paper is out in Socio-Economic Review! doi.org/10.1093/ser/... Using firm-level data on all stock listed firms in the world I show that it is not the growth of shareholder remunerations that causes rising payout ratios, but precisely their inability to fall, their downward rigidity.

Abstract. The rise of payout ratios has been ascribed by financialization scholars to shareholder value orientation (SVO), a governance practice associated